The Only Stakeholder Who Benefits from India's Public Sector

- In this issue:

- » Will 2016's Mega Spectrum Auction find bidders?

- » Signs of recovery in the corporate balance sheets

- » Round up on markets

- » ...and more!

Bleeding public sector undertakings (PSUs) have accumulated more than a trillion rupees of losses in the past year. But none are getting privatised in a hurry. And if you are wondering whether the government will try to revive them, put your doubts to rest. These words of Prime Minister Modi say it all:

The government just offered a generous revision in pay to PSU employees based on recommendations from the Seventh Pay Commission. And that does not surprise us. It is just one of the ways to keep the PSUs running.

But as an investor, you must have one question on your mind: Which stakeholders do the PSUs benefit the most?

You don't need me to tell you that PSUs do not offer the best return ratios to their shareholders. Unless you buy the strongest and most cash-rich PSUs really cheap, you may get a raw deal. Cash-rich PSUs will at least pay out hefty dividends. And the largest and most monopolistic PSUs will always have the government's backing. These benefits aside, though, PSUs do not really favour shareholders.

Unlike the aviation and retailing industries, PSUs do not always offer their customers the best deal. Rather, most PSUs can't compete with the products and services of their private sector counterparts - Air India being a case in point. So it is not as though the customers benefit at the cost of shareholders. No, customers certainly aren't the happiest stakeholders of PSUs.

We would like to believe that the employees of government enterprises have it all. The labour laws and trade unions protecting employment at PSUs make it easy for them to be inefficient. The average productivity and profitability per employee at most PSUs pale against that of their private competitors. And yet, their pay keeps going up with every Pay Commission recommendation. But despite this, the most talented graduates in the country do not aspire to join the public sector.

That's partly due to the huge gap between the remuneration of the top management at public and private sector entities. Take the salary of the CEO of any PSU - be it a bank like SBI or a power a company like NTPC. The salaries of the chiefs of these behemoths have been as low as one-twentieth of the private sector CEOs. Family-run private sector entities are known to pay their management top dollar salaries. But the huge gap in the management compensation levels at PSUs and private sector is inexplicable.

The only stakeholder who seems to be indifferent to the problems at PSUs is the employee at the lowest rung of the institution. The PSUs are among the biggest employment providers in India. In 2015, they employed about 9 million people. The railways employ about 1.3 million. SBI, with all its associates, employs about 0.2 million. The other PSUs (listed and unlisted) are equally good employers, if not paymasters. They offer job opportunities and job security to millions. This makes PSUs politically sensitive and forces the government to make policies that favour the employees.

Can a growing economy like India afford to lose a trillion rupees of tax payer money to pay salaries at loss-making PSUs? I guess the question is rhetorical. And it's been answered several times before anyway.

The real problem is that most of us do not understand the implications of this all wasted taxpayer money on the long-term prospects for the economy.

It's true that, over the past few years, crony capitalism has taken a beating. But my colleague Vivek Kaul believes that crony socialism is now alive and kicking.

And if you think we've always had this problem...well, you are in for a surprise.

To know the details, download Vivek's Special Report - The Crony Socialism of Narendra Modi.

Do you think the government's intent to keep even the loss making PSUs going is a case of Crony Socialism? Let us know your comments or share your views in the Equitymaster Club.

| --- Advertisement --- Profit From Junior Blue Chips... We have released our latest Special Report on the best of the best small caps - Junior Blue Chips! Yes, we believe Junior Blue Chips possess the high growth potential of small caps along with the stability of blue chips. That is an amazing combination every investor would want in his portfolio. And the best part is you can get this report for FREE! Just click here to know how... ------------------------------ |

03:10 Chart of the day

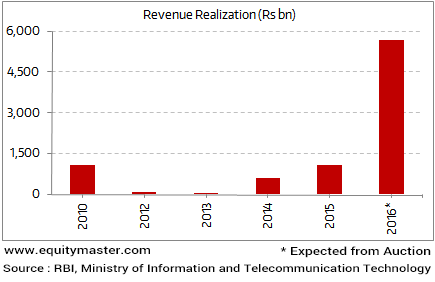

The government recently cleared the biggest ever telecom spectrum auction. The total value of the airwaves up for sale exceeds Rs 5,000 billion!

Historically, these auctions have largely been exercised by the well established players in the telecom industry. Companies such as Bharti Airtel, Vodafone and Idea Cellular have shelled out huge sums in order to succeeded in availing the spectrum license. The last spectrum auction in March 2015 was a big success. The government garnered bids of about Rs 1,100 billion. But things have completely changed in last one year.

Will the Mega Spectrum Auction be a Flop Show?

Unlike last year, none of the telcos have to renew any of their spectrum soon. Thus, there is no compulsion to bid to ensure that their operations will continue. There's also the question of debt. Last year, the balance sheets of telcos were stretched. But they still had a little room left to borrow some more. This they certainly did, taking advantage of the government's new deferred repayment clause. The result? They got all the spectrum they wanted. But at the same time, pushed their leverage ratios to the limit. Under a gigantic debt burden of US$50-60 billion, telcos are in no position to repeat their extravagant bidding this time around.

The things have been more downhill than uphill for this sector since some time now. The government and the regulator have been milking the sector's resources for a while.

But this time around, one companies have lower appetite to finance these expensive auctions. And looking at the past auction, it seems very unlikely that the government's ambitious plans are going to succeed this year.

Talking about debt, here is some good news.

The latest Financial Stability Report (FSR) was recently released by the Reserve Bank of India (RBI). The report offers some hope of improvement in corporate balance sheet. The subset of companies that fall into 'leveraged' category have declined in the past six months. The report cites...

- The overall risks to the corporate sector, which increased after the global financial crisis during 2007-08, have shown some moderation in 2015-16.

The leveraged category comprises of the companies that have a negative net-worth or debt is two times more than its equity.

Readers would well recollect that most of this repair work started when banks were directed to classify stressed assets as bad loans. RBI's asset quality review (AQR) had put pressures on the banks profitability. Thus, in order to limit the hit on their balance sheets, banks have pushed companies to sell assets. This is believed to be an important reason for decline the corporate debts.

But how will things pan out going forward? This depends on RBI's policies on bad loans. And the new governor, who will soon be taking charge, will have an important role to play.

After opening on a positive note, the Indian indices have continued to surge upwards. At the time of writing, the�BSE Sensex�is trading higher by 202 (up 0.75%) and the�NSE Nifty�is trading up by 58 points (down 0.71%). The�BSE Mid Cap�index is trading up by 0.88%, while the�BSE Small Cap�index is trading higher by 1.32%.

04:50 Investing mantra

"You don't need to be a rocket scientist. Investing is not a game where the guy with the 160 IQ beats the guy with 130 IQ." - Warren Buffett

This edition of The 5 Minute WrapUp is authored by Tanushree Banerjee (Research Analyst) and Bhavita Nagrani (Research Analyst).Today's Premium Edition.

How Is the Current Fiscal Shaping Up for Auto?

While FY16 was a mixed year for the auto industry, the first two months of FY17 have seen it fly off to a good start.

Read On...

| Get Access

Recent Articles

- All Good Things Come to an End... April 8, 2020

- Why your favourite e-letter won't reach you every week day.

- A Safe Stock to Lockdown Now April 2, 2020

- The market crashc has made strong, established brands attractive. Here's a stock to make the most of this opportunity...

- Sorry Warren Buffett, I'm Following This Man Instead of You in 2020 March 30, 2020

- This man warned of an impending market correction while everyone else was celebrating the renewed optimism in early 2020...

- China Had Its Brawn. It's Time for India's Brain March 23, 2020

- The post coronavirus economic boom won't be led by China.

Equitymaster requests your view! Post a comment on "The Only Stakeholder Who Benefits from India's Public Sector". Click here!

9 Responses to "The Only Stakeholder Who Benefits from India's Public Sector"

allen

Jul 3, 2016PSU bashing is a favorite theme of the press. But is our Private sector any better? They want loans for free from the Govt banks, try their best to avoid paying taxes. The very biggest among them like TATA and Birla are more interested in investing abroad than India. FE market has punished them for that.Process industries in Pvt sector like cement chemicals, fertilisers,power generation are efficient, alongwith pharma and IT. High tech manufacture is not a success in their case. To develop high technology in missiles , power equipment, ship building Govt has to rely on the Public sector. The post and telegraph dept and railways have served INdia well. Govt should progressively privatise these areas. INdian products both pvt and public sector are low tech and of poor quality. Govt should be more open to FDI.

ravisankar

Jul 3, 2016Agreed the pay commission is not applicable to PSU. But does it mean the salary of PSU employees will not be matched?

Pay commission is the trend setter and the PSU and all state governments follow it

State government employees are not included in pay commission and that does not mean they are getting less than central government

So I find nothing wrong in this article as mentioned by others.

ravi

Jul 2, 2016Your website is not practical in approach.You concentrate more on news like items.Your site looks more like a financial magazine.

Balakrishnan R

Jul 1, 2016Hi Madam,

The present pay revision is applicable only to government employees, Army, Navy, Air Force staff like. It is not applicable to employees of PSUs. They come under company law and they don't pension. As you have written, there is a huge in the pay packages of CEOs of PSU and Private sector. Irrespective of this some PSUs are making profit even in competitive environment. As you know RBI governor's salary is less than Rs 2 lakhs. The pay of CEO of ICICI Bank may be several times of RBI governor's salary.

V Thiruvalluvan

Jul 1, 2016The sevneth pay commission is for the Government employees Not for the PSUs

Manish Shah

Jul 1, 2016I most emphatically agree that the Governments intention of keeping all loss making PSUs going is a clear case of Crony Socialism....

S.A.Narayan

Jul 1, 2016The author has got her facts a little confused. The public sector in India comprises direct govt depts, where the employer is the central or state govts (posts and telegraph, govt depts, railways etc). Then there are the companies which are either listed or unlisted. In the companies(registered under the companies act/banking companies act), the govt, either central or state is the majority shareholder. The 7th pay commission increases are given only to the direct govt employees, and pensioners at all levels. In the case of govt owned banks separate pay committees decide increases for officers and negotiated settlements with collectives by Indian Banks Association decide pay increases for bargainable categories(both public and pvt banks). In the listed and unlisted PSUs again separate pay committees recommend pay increases for officers and negotiated settlements with unions decide increases with individual/group companies.

Krishna Rau

Jul 1, 2016I have been keenly following your daily posts. I appreciate most of it. I am otherwise in agreement with you on why PSUs function the way they do. But it is a bit out of place to link it with the 7 CPC recommendations. The 7CPC is for Govt employees and not for the PSU employees.

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Prasad RK

May 14, 2017One of the most detestable comments a compatriot can give to another! Shouting at top of their voice are the barons of Private Sector...whose top rung of people draw 10,000 times more salary than the lower rung people...just for a simple reason that they are the masters! The blood-suckers of humanity within their own community try to showcase Air India as a case of poor services to customers......but the same people happily get thrown down from a plane in their dreamland...without murmuring a word!

Crap....

Crap.....

Crap....