MEMBER'S LOGINX

| Invalid Username / Password | ||||||||

| Invalid Captcha | ||||||||

|

||||||||

| Sign Up | Forgot Password? | ||||||||

- Home

- Views On News

- Jan 8, 2023 - Stocks that Could Double Sensex Returns From 2023

Stocks that Could Double Sensex Returns From 2023

More than two thirds of the listed companies in India have been undertaking technology - led capex over the past few years.

Even the RBI capex data and company annual reports point to this fact.

In 1970, Asian Paints bought a mainframe computer for Rs 80 million (m). It thus became one of India's first private companies to own one.

Since then, the company has digitised its inventory and billing management, which helped save time and costs.

By the end of the decade, Asian Paints started using computerised colour tinting machines. The company also trained employees to use personal computers in the 1980s and established a customer care helpline in the 1990s.

From centralised order booking to supply chain management to storage and retrieval systems were automated in 2008.

So, for more than 50 years, Asian Paints has been collecting data on the colour, size, and quantity of paints purchased all over India. They continue to store proprietary data on paint demand for each neighbourhood. This allows the company to predict paint demand well in advance.

Recently, the company implemented state-of-the-art automatic truck-loading systems in the two new plants at Mysuru and Visakhapatnam. They also use advanced artificial intelligence (AI) and machine learning (ML), to constantly improve the overall demand forecast.

I now see several companies going the Asian Paints way.

Yes, it's true. More than two thirds of the listed companies in India have been undertaking technology-led capex over the past few years. Even the RBI capex data and company annual reports point to this fact.

There is a sharp increase in the share of intangible assets (other than goodwill) in the balance sheets. And the rise in the share of R&D expenses has hardly been witnessed earlier.

Sceptics may want to dismiss these data points as one-offs in the post pandemic recovery phase. But they couldn't be more wrong.

Here again, there are several data points that suggest the capex will continue. More so, the technology related ones.

First of all, India's corporate profits to GDP at 4.5% is currently at a decade high. Though last seen in 2012, the sharp rise in earnings is backed by healthy balance sheets rather than macro tailwinds.

Average operating margins, currently at 16.7%, were last seen in 2005. The average net margin of 8.7% was last crossed in 2011.As companies were left loaded with debt in the previous capex cycle, there were few capacity additions in the past decade.

This time around, India's corporate debt to GDP ratio, at about 60%, is significantly lower than the global average.

Neither have companies splurged on expensive inorganic growth. Nor have they kept their balance sheets leveraged. On the contrary, most chose to get leaner during the pandemic by paying off debt obligations.

What is more, the lenders themselves are in good financial health. Not just private sector, but even public sector banks have seen profits soar in the past few quarters.

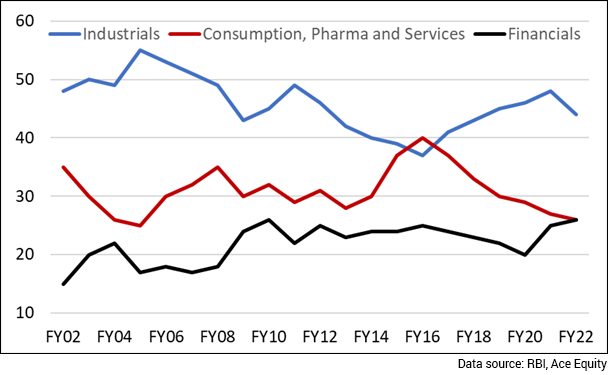

Banks and NBFCs' Share of Corporate Profits at Decadal Highs

Do note that India has moved from a US$300 billion (bn) economy to US$3 trillion (tn) in 30 years. The vision is to become a US$10 tn economy by 2031.

This transformative journey is backed by multiple growth vectors like broader demand from consumption with adequate support from the lower cost of capital and a proactive policy stance from the government.

The reason I believe capex will be a game changer is because this time it is a vital cog in India's transformation.

Gross fixed capital formation (GFCF) forms around 30% of India's GDP at US$790 bn. Public and private capex are stronger, while infrastructure and industrial capex were flat over the last decade.

India has witnessed a sluggish investment cycle for the past 10 years since peaking in FY11, following the recovery from the Global Financial Crisis (GFC).This was characterised by the absence of large-scale capex in sectors such as power and metals.

Of the US$790 bn total GFCF, around US$325-350 bn is in large-scale organised capex on industries (US$200 bn) and infrastructure (US$125 bn) that are identifiable capital investment opportunities.

The post-covid demand recovery, higher commodity prices, and better pricing power driven by industry consolidation are among the key drivers.

Industry utilisation is at a trigger point (73.4%, highest in the last 12 quarters) for the top five players in most of the core sectors - cement, metals, power, and refining - making a strong case for corporate capex.

Order inflows based on recent data suggest a healthy three-year CAGR of 11-12%. Short-cycle revenues of machinery and consumables, and capital goods imports suggest that the investment cycle build is strengthening.

What is different this time?

Diversity of demand: India is witnessing multiple tailwinds in terms of higher consumption, at inflexion GDP per capita of $2200+, better factor cost dynamics (on personnel, money, material), post-pandemic resumption of the economy, emerging opportunities to plug in the business value migration opportunities from the global supply chains like China+1/Europe+1.

Prudence towards capital allocation: The higher size of the economy makes this capex cycle interesting. It is also outcome-centric, efficiency-focused and prudent in allocations. Thus, the economy offers a good local anchor for every asset creation that targets a concurrent opportunity to play the global supply chain value migration.

In the past cycles, commodity inflation and negative real interest rates had led to leveraged corporate capex upcycles. This was also accompanied by crony capitalism, reckless investments, and substandard underwriting. Now, it is replaced with a focus on economic profits, prudent underwriting, cash generation and cash reserves for the corporates.

Global Geopolitical Conflict: While the Russia-Ukraine war did affect supply chains in general and commodity costs specifically, it has accelerated trends such as alternatives to the existing overdependence on a single geography. India with its scale established industrial base, and a knowledge-based service economy that respects intellectual property is well poised to participate in this space.

The post-pandemic urgency of localisation has further increased the relevance of some of the large MNCs to leverage their Indian subsidiaries in the global supply chains (R&D, products, solutions). Global engineering companies such as Cummins and ABB also indicate strong momentum for capex in their end markets.

The top 10 corporate groups are set to invest over US$150 bn in multiple sectors within India. The banking system is in better health in terms of systems, capital adequacy and ready access to buoyant local capital or long-term-oriented global capital to fund this growth.

Better Policy Support: The government is playing its part with a policy framework that is incentivising productive capital formation, catalysing new investments with a proactive pro-business and pro-reforms stance. It is also signing multiple bilateral trade deals with large markets like Australia, UAE, and many more.

There are two core drivers of capex in the near term, the government of India National Infrastructure Pipeline (NIP) and the capex plans of the private sector. In the NIP, roads, railways and power are some of the main drivers of capex plans.

The private sector capex plans are across the board with special focus on renewable energy and PLI-driven capex in mobile, solar, Electric Vehicle, battery technology, automobiles, pharma, among others.

India witnessed a solid capex upcycle in 2003-2007. During this phase, the Sensex was up seven times. But the actual stocks riding the capex cycle went up 15 to 20 times during this phase.

If you go by the current commentary of bank managements, the capex cycle of 2020s is already here. There is a guidance of corporate credit growth. Investment activity is gaining momentum.

From a broader environment perspective, there are policy tailwinds. The boost from indigenisation and increase in budget allocations is already evident on India's top defence stocks.

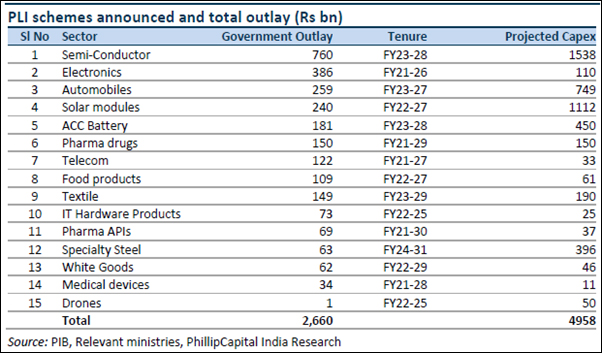

In the 2022 budget, the government hiked its capex by 35% to Rs 7.5 tn...the number could go higher in the 2023 budget. The PLI schemes have been set in motion. This alone could have huge multiplier effect for private sector capex.

From a bottom-up perspective, corporate balance sheets are cleaner with debt-to-equity ratio looking good. The operating cash flows are higher too. The banks have a cleaner balance sheets as well and are geared up to lend more.

The capacity utilisation of corporate India is up from 68% to 74%. The sectors at the forefront of this capex revival include road, rail, port in, cement, logistics, oil and gas, renewables, power sector, defence, auto, pharma, chemicals, and textiles and more.

Then there are structural tailwinds. The global companies are looking for outsourcing beyond China. If India is a beneficiary of even a fraction of the demand, it could be a huge incremental growth over our existing base.

Therefore, even as the world grapples with high interest rates, both Indian corporates and their lenders are well equipped to take the risks in their stride. Major systemic risk due to the capex boom is almost ruled out.

So, as an investor, the least you could do is ensure the companies you own are doing their bit in riding the capex boom. They should not only be allocating their capital judiciously but also use the rise in cash flows and profits to build up capacities.

Doing this will ensure that your stocks offer no negative surprises in earnings in 2023 and beyond.

Tanushree Banerjee (Research Analyst), is the editor of Stock Select and Forever Stocks. Tanushree started her career at Equitymaster covering the banking and financial sector stocks and scrutinising RBI policies. Over the last decade, she developed Equitymaster's research processes that helped us pick out various multibaggers, across all sectors. A firm believer of "safety first" when it comes to investing, Tanushree closely follows the investing philosophies of Warren Buffett, Jeremy Grantham, and Joel Greenblatt.

Equitymaster requests your view! Post a comment on "Stocks that Could Double Sensex Returns From 2023". Click here!

1 Responses to "Stocks that Could Double Sensex Returns From 2023"

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

H M PRABHU

Jan 11, 202309844025697

Good one Tanushree!! Succinct read on big picture driving the economy for India. Thanks for the capsule.