Is it Time to Go Back to Value Investing?

Over the past one month, every night from Monday to Friday, my family and I have been hooked on to Shark Tank India.

The innovative ideas coming from every part of India with such limited means is fascinating to say the least.

Seeing the pace and zeal of innovation, it won't be long when India will be called the land of dreams and opportunities.

After all, we have the best demographics in the world thanks to our young population. And we Indians are known for their 'Jugaad' mind-set.

However there is one thing that makes me uneasy every time I watch the show. If you've have been reading my articles, you might guess which aspect of the show I'm referring to.

It's the valuations at which these start-up companies on Shark Tank are initially valued by the entrepreneurs making the pitch. It's baffling to see how the valuations are cut by almost half in many cases by the Sharks.

On a lighter note, the valuation of companies which some of the sharks own, too deserve to be cut by more than half.

I find it uncomfortable when entrepreneurs like Ashneer Grover talks about profits when Bharat Pe's losses are just growing manifold.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

----------------------------------------

Never mind. Let irrationality prevail for some more time.

After all, if Ashneer Grover's Bharat Pe can spend Rs 2.3 bn to generate a revenue of Rs 60 m, then all these young SME and MSME entrepreneurs have a right to ask for such lofty valuations.

In this circus of massive liquidity and low interest rates, the start-up bubble is getting bigger.

And the repercussions are going to be massive when the bubble pops.

In fact, the bubble has already started to show signs of popping looking at the stock prices of Paytm, CarTrade, Zomato, and Policy Bazaar.

In my previous articles, I have written enough about why I don't like loss making tech IPOs. I cautioned readers after these listings and even after the 30-50% fall in most of these stocks.

The valuations of the listed as well as the unlisted companies will get butchered when interest rates go up and free money from Santa Claus, the US Federal Reserve, comes to an end.

The dilemma that investors face these days is...

a) Jump on the bandwagon of price and momentum

b) Focus on value

The tug of war between growth and value has been going for many years.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

What You Need to Know Before Investing in Small Businesses

Read this letter before you invest in small companies

Read Now

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------

A part of the last decade belonged to growth while the other to value. The last couple of years belonged to growth, while value stocks lagged.

However, things are changing...

Let's look at the US market.

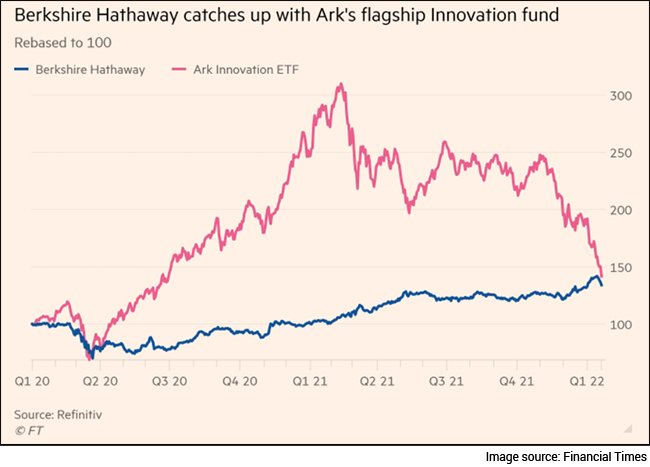

Cathy Woods (Growth) V/s Warren Buffett (Value)

Cathie Woods' ARK innovation fund takes aggressive bets on high growth disruptive companies. It beat a majority of its competition in 2020. This led to its asset under management growing to US$61 bn at its peak.

However, the past 6 months have been characterised by outflows from ARK Invest. In fact, the fund has tanked 45% since the start of 2022.

Definitely not a pleasant new year for Cathie Wood.

On the other hand, legendary investor Warren Buffett's Berkshire Hathaway, a flagbearer of value, has bridged the gap. In fact, he is up 2% since the start of 2022.

ARK Innovation Fund Back to Square One

While Cathie Wood was hailed as the modern day Warren Buffett, we all know who will have the last laugh.

I'm ready to put my neck out and bet on value over the next couple of years.

My conviction is based on the fact that a growing company's stock tends to have its PE ratio re-rated higher.

The whole assumption of higher growth is based in an environment when the macro environment supports it i.e. is low interest rates and high liquidity.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

This Silvery-white Metal is a Potential Fortune Maker

This silvery-white metal goes inside almost all the electronic gadgets that you use: mobile phone, laptop, Bluetooth speakers.

Not only that... this metal also goes inside equipment used by large data centres, telecom towers, railways, planes, EVs.

We're talking about Lithium. Lithium is the new oil.

Our research has found the best way to tap into this rising demand of lithium in India.

See Details Here

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------

Investors generally pay a higher premium for growth. This is because we tend to extrapolate the present into the future much more than it's feasible.

You must have heard this saying, 'As long as there is growth, any multiple is justified'.

In today's slang, it's called BAAP - Buy at any Price.

Now let me show you how a stock can de-rate like a falling knife when growth disappoints even marginally.

The Jubilant Foodworks Stock Crash

When same store sales growth (SSSG) was strong and beating the consensus estimates, the market gave Jubilant Foodworks, a forward PE ratio of 80 times.

Every increase in the PE ratio gave the stock price a strong upside. There always comes a point when growth starts to moderate. After all, no company can outsmart its own environment.

So when growth slows down mildly, the stocks with astronomical PE ratios crash as if there is no tomorrow.

The same happened here in January. Growth slowed down marginally with respect to the market's expectations. The stock fell 25% in less than a month.

The thumb rule is to be wary of high PE stocks without super normal growth.

So why I think value investing will be back in flavour?

To understand why value will be back in flavour, let us look at why growth will be out of flavour.

Rising Interest Rates: Biggest Party Spoiler

Low interest rates leads to high liquidity, which leads to easier access to credit, which leads to higher demand, which leads to higher inflation, which leads to higher interest rates.

Here's some food for thought. A barrel of crude oil in 2008 at its peak was trading at US$148 with an exchange rate of Rs 43/$. That comes out to a crude oil price of Rs 6,364 per barrel.

Today, crude oil is at US$90. It hasn't reached the peak but the exchange rate has climbed to Rs 74/$. This translates in to a per barrel cost of Rs 6,808.

Imagine the inflation it has already added and is likely to add if the price touches US$100 or more.

During such times, money shifts to stocks which have a margin of safety in valuations.

In a rising interest rates scenario, the pecking order should be as follows.

# Choice 1: Cheap valuation + Growth prospects

# Choice 2: Fairly valued + Growth prospects

# Choice 3: Richly Valued + Very strong growth prospects

Completely avoid the following stocks:

- Very high valuations: PE in excess of 50-60 or P/B in excess of 6-8.

- Growth: Historical Growth at 10-15%.

With the rising interest rates there is no way you can justify holding these stocks.

In conclusion...

In an inflationary environment pick the producers and not the consumers.

Warm regards,

Aditya Vora

Research Analyst, Hidden Treasure

PS: If you're a retail investor and interested in making VC-like returns, click here for exciting opportunities.

Recent Articles

- Stocks Profiting from the Rise of the Luxury Class in India April 26, 2024

- These stocks benefit the most from the growing opulent class in India.

- A Rare Opportunity to Profit from Pharma Stocks April 25, 2024

- This opportunity can create a lot of wealth. Keep an eye on it.

- Why CE Info and Netweb Technologies Can Go Where NVIDIA Can't... April 24, 2024

- A 100-day programme will look for companies that can fortify India's deeptech foray.

- Can Your Stocks Benefit from Higher Inflation? April 23, 2024

- Higher Inflation is good for these companies.

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "Is it Time to Go Back to Value Investing?". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!