IRFC: A Realistic Assessment of its True Value

Imagine that you are the owner of a business where the net worth is Rs 100 crores and the profit is Rs 15 crores.

That makes it a business that has a return of 15% or to be more specific, a business where the return on net worth is 15%.

Now, also imagine that this business has been growing its profits by around 12% every year. So, if its profit was Rs 15 crore this year, it will make a profit of Rs 16.8 crores next year.

A growth of 12% on 15 crores is Rs 1.8 crores and hence, Rs 15 crore profits will become Rs 16.8 crores next year and so on. Now, this extra 12% profits doesn't come out of thin air.

It comes from the company having to make an extra investment.

Let us understand this better with the help of this image.

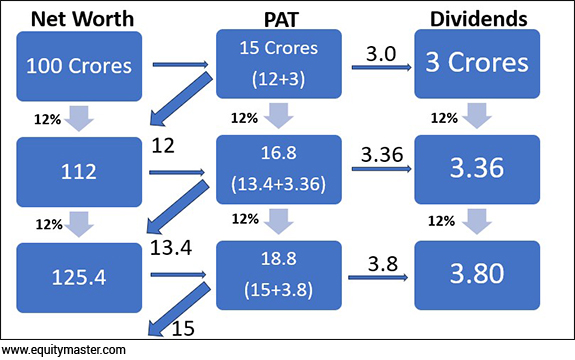

The Growth Cycle

Well, at first sight, the slide may look intimidating because there are a lot of things that are happening here.

But trust me, it is very simple.

So, we start with the top left corner of the image. The net worth column.

The company has a net worth of Rs 100 crores. It earns a profit of Rs 15 crore which is shown as PAT to the right of the net worth column. So, Rs 15 crore profit on Rs 100 crore becomes a return of 15%.

Now, out of this Rs 15 crore, Rs 12 crores will be invested back into the business. This is because we want the profits to grow by 12% and therefore, we will have to increase the net worth by 12% which comes to Rs 112 crores.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

Did you miss this the last time?

Back in 2003, a powerful Economic Force was in action that led to the small cap index growing by nearly 1600% in 5 years.

After disappearing for more than 10 years, this Economic Force has finally returned!

Discover how to take advantage of it by clicking below

I'm interested

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------------

The remaining Rs 3 crores profits out of the 15 crores will be paid out as dividends, which is the last column in the slide.

So, let me repeat that again.

The business has a net worth of Rs 100 crores. The return on equity is 15% and therefore, a profit of Rs 15 crores. Then, out of this Rs 15 crores, Rs 12 crores is earmarked for growth and the remaining 3 crores is paid out as dividends.

Now, moving on to the second row. The new net worth of Rs 112 crores will again a generate a profit of Rs 16.8 crores based on 15% return on equity.

This Rs 16.8 crores will be split into Rs 13.4 crores, which will be invested back into the business for 12% growth and another Rs 3.36 crores which will be again paid out as dividends.

Coming to the last row, we have a new net worth of Rs 125.4 crores, which will produce a profit of Rs 18.8 crores.

Out of this Rs 18.8 crores, Rs 15 will be earmarked for 12% growth and Rs 3.8 crores will be paid out as dividends.

And this will continue to go on for many years.

This is a simplified version of how it works in the real world but the basic principles are the same.

A company earns a certain return on its net worth, which is known as the PAT or the profits. Then based on the growth projections by the management, a large part of the profit is invested back in the business to buy plant and machinery or to invest in working capital. The remainder of the profit is then paid out as dividends.

I hope you understood the basic nuts and bolts of how a company earns profits and how it grows.

Now let us try and value such businesses. If I have to arrive at the valuation of the simple business we just discussed, what do you think will be the right valuation to pay for this stock?

Well, you will use the following simple formula.

Value = Dividend/(R-G)

Here, dividend is the dividend that will be paid out the next year, R is the required rate of return, the return that you want the stock to earn. G stands for expected growth rate, which in our case stands at 12%.

I am not going to go into the details of the formula. There is plenty of material available on the internet and you can check that out. All I want you to remember right now is the formula.

Now, let's change this formula a bit.

Value = Book value* (RONW-G)/(R-G)

Dividend is nothing but book value of the company multiplied by its return on net worth minus growth.

Let's check whether it is correct or not.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

Worried About Stock Market Volatility During Election Season?

Grab our Safe Stock Research at 60% Off

Full details here

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------------

Our business had a net worth of Rs 100 crores in year 1 if you remember. It had a return on net worth of 15% and a growth rate of 12%.

If you subtract 12% growth rate from 15% return on net worth, you get 3% which when you multiply by Rs 100 crores which is the net worth, you get Rs 3 crores.

This Rs 3 crores is nothing, but the dividend paid out that year.

So, our formula that dividend equals book value multiplied by return on net worth minus growth rate is indeed correct.

Now, putting the values of book value, return on net worth, growth rate and required rate of return into the formula gives us a value of 1 times book value.

So, the value of our company is nothing but its book value which is Rs 100 crores. So, if you are looking to buy this business and your expected rate of return is 15%, then you should pay no more than Rs 100 crores to buy the business.

You can certainly play around with this formula by assuming different values for return on equity, required rate of return and long term growth.

This formula is also very sensitive. This means that even a small change in any of the parameters can change the value a great deal.

However, don't worry about its sensitivity too much. Because we are not looking for scientific precision here. We are only looking for rough approximation.

Now, let's try and apply the same formula for valuing one of the hottest stocks these days i.e. Indian Railway Finance Corporation or IRFC as it is popularly known as.

The stock which was trading at close to Rs 30 few months back, has more than doubled and now trades at close to Rs 73 per share.

However, is Rs 73 the true value of the stock? Let us find out using the formula. The book value of IRFC is around Rs 36 per share. It's average ROE over the last few years stands at close to 15%.

Let us assume our rate of return to be 15% and the growth that it is expected to log in over the long term to be around 12%.

If you plug in all these numbers into the formula, you get a value of 1 times book value. Yes, that's correct. As per this formula, the company's true value is not more than 1 times its book value which is around Rs 36 per share.

Make: Your Investing Stress-free with Value for Money Stocks

This means that if someone wants to earn 15% on the stock over the long term, his buy price needs to be Rs 36 per share or lower.

To put it differently, the stock is currently twice as expensive than what the formula is suggesting.

This gives rise to an important question. Why is the market willing to pay a 100% premium for IRFC over its value as determined by this formula? What is the market seeing that we are not? Or is the market being too optimistic about the stock's future?

To be honest, our formula assumes that IRFC is an average Indian company with average ROE of 15% and long-term growth rate in line with how the Indian economy has grown historically.

But the valuation that the market is giving seems justifiable on the grounds that the market thinks that it is a special company.

A special company either has return on equity that's much higher than the average company or it has a growth rate that's much superior than the average company.

Take Bajaj Finance for example. It is trading at almost 7x its latest book value. Now, whether that's cheap or expensive is something we can discuss later. But it is not an average company based on its financial performance.

The company's bottomline has grown at an impressive 32% CAGR over the last five years and its return on equity has averaged almost 20% during the same period.

This means that it has proven itself and hence, deserves a valuation of more than 1 times book value that the formula seems to be suggesting for IRFC.

IRFC on the other hand, has shown no such impressive performance. It's bottomline has grown at a CAGR of 10-12% over the last five years and return on equity is also close to 15% per annum.

Therefore, if we assume the same ROE and growth rate going forward, the value comes to 1 time book value, which is around Rs 36 per share.

However, what if the stock has been an average quality stock in the past but has all the makings of a good quality stock in the future. Should you not give it a higher valuation if its future appears bright than the past?

Well, we should but we would also be going against the tenets of conservatism if we do that.

You see, around 80-90% of the companies out there are average or below average companies. Only 10% of them are above average or good quality companies and even that number could be an exaggeration.

Therefore, whenever one is valuing a company, one should always proceed with the assumption that one is buying an average stock and value it accordingly.

This way, if it turns out to be a good quality stock, then there are huge multibaggers gains for the taking.

But if it doesn't, then your downside is also limited because you never paid for quality in the first place.

But if you pay for quality upfront and it does not turn out to be that way, then the downside could be huge.

You see, we investors tend to overestimate ourselves.

We tend to believe that we have some special ability to spot quality stocks that other investors don't and under this misconception, we may end up overpaying.

However, if we move forward with the assumption that we don't have any such ability then we will seldom overpay and this way, keep our downside to a minimum.

I have found this to be a much better approach over the long term and always try to stick to it.

Thus, IRFC may be a quality stock and it could be undervalued even at the current valuations as per a lot of investors.

However, a conservative investor wouldn't tend to think so. He will find the risk-reward ratio against him and will opt to stay away from the stock.

I hope this piece went some way in clearing your doubts about IRFC as an investment.

Happy Investing.

Warm regards,

Rahul Shah

Editor and Research Analyst, Profit Hunter

Recent Articles

- Is This the Best PSU Stock in the Market? May 21, 2024

- This little-known PSU stock is making waves in the data centre market.

- Is Tata Motors Still a One-Trick Pony? May 20, 2024

- Decoding the new era of Tata Motors.

- Rebound Overdue in Top Hidden Fintech Stocks May 17, 2024

- Recent RBI penalties have skewed the valuation metrics in India's financial sector.

- Indian Solar Stocks: Impact of the US China Tariff War May 16, 2024

- The second order effects of US China trade war.

Equitymaster requests your view! Post a comment on "IRFC: A Realistic Assessment of its True Value". Click here!

5 Responses to "IRFC: A Realistic Assessment of its True Value"

Tapan Mukherjee

Sep 13, 2023An aptly titled article. It's logic and clarity is simple - in true 'Rahul' style. Many thanks.

Apoorv

Sep 12, 2023Very apt and timely article! Which instills some sense and rationality into mind of an average investor like may of us who might commit the said mistake under fomo and regret later when the froth is cleared.

Francis D'cruz

Sep 12, 2023Good and very logical advice. Actually advice clears the mind and helps to take a clear decision. Thank you.

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Lakshman Kumar

Sep 13, 2023Well explained about True Value with an appropriate example. Done so, is the present price right to exit the stock?