How Investors Lost Money on the Greatest Event in India's Economic History

- In this issue:

- » Investors in mutual funds moving from equity to debt

- » Have we reached 'peak gold'?

- » Round up of today's market

- » ...and more!

Do you think that whenever good things happen to the economy, equity investors make money?

Well, you are wrong.

No matter how good the event.

Take the greatest event in India's economic history for example: The 1991 liberalisation of the Indian economy. We just celebrated 25 years since that hallowed moment when then Finance Minister Manmohan Singh presented the budget before Parliament on July 24, 1991. It was the budget that kicked off the reforms.

If India's modern economic history has to be pinned down to the single most important event, this was it. These reforms changed the way India lives. In effect, it took us from living like ascetics to being spoilt for choice in every area of life.

When the reforms were announced, investors were quick to realise what was in store for the Indian economy. Naturally, they were excited.

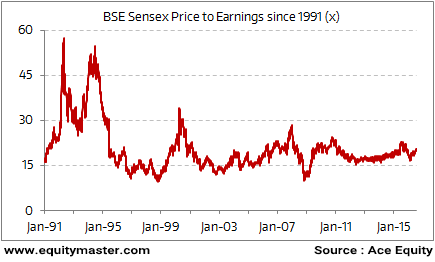

In fact, if the stock market was any indicator, 'excited' would be an understatement. Elated about the prospects that lie ahead for the economy, and further spurred on by 'big bull' Harshad Mehta, the BSE Sensex went on to see a price-to-earnings multiple (PE) of more than 55 times.

Well, the reforms delivered. They brought on all the anticipated benefits to the economy over the next 25 years, and more.

The stock market, though, would never see such a valuation again. Not even close.

Here, have a look:

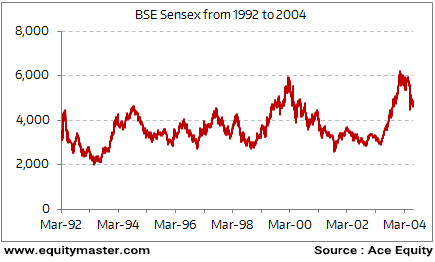

And investors who bought into these overheated markets in the name of liberalisation were in for a rude shock. The stock markets would trade at or below that level for a large part of the next twelve long years. At times more than 50% lower:

In their excitement, all calculations had gone out the window. Investors were willing to pay just about anything to get their hands on stocks. And when that happens, disaster - almost always - is just around the corner.

Benjamin Graham summed it up...way back in 1972:

- The habit of relating what is paid to what is being offered is an invaluable trait in investment. In an article in a women's magazine many years ago we advised the readers to buy their stocks as they bought their groceries, not as they bought their perfume. The really dreadful losses of the past few years (and on many similar occasions before) were realized in those common-stock issues where the buyer forgot to ask 'How much?'

Be it liberalisation, a new government, GST or a great monsoon, you always got to ask the all-important question: Everything said and done, am I paying too much for the stock in relation to its intrinsic value?

For even though the company may turn out to do very well, or the economy may have some great years ahead of it, when you pay too much, even a good stock can quickly turn into a bad investment.

How important do you consider valuations in investing? Would you pay anything to get your hands on a stock with great prospects? Let us know your comments or share your views in the Equitymaster Club.

| --- Advertisement --- The Way To Small Caps For eight years, we at Equitymaster have made it our business to find solid small caps... And what do we have to show for our effort? Recommendations that generated returns like 250% in 2 years, 217% in 3 years 11 months, 288% in 2 years 5 months, 133% in 1 year 3 months! Of course, past performance does not guarantee future returns...And you need to keep that in mind. But the fact remains our research process remains the same... And now you too could receive our recommendations... Interested? Click here to know more... ------------------------------ |

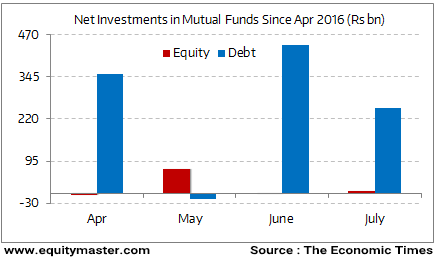

02:50 Chart of the day

If today's chart of the day is any indication, looks like investors have rekindled their romance with bond funds. As the chart highlights, close to a whopping Rs 70 bn have been poured into debt funds by investors since June 1, 2016. In comparison, equities have attracted investments worth a paltry Rs 4 bn during the same period. In fact, even the couple of months prior to that, debt funds have garnered significantly higher inflows than their equities counterpart.

The reason? Well, the old habit of looking into the rear view mirror and not the windshield. Experts contend that since debt funds have given better returns than equity mutual funds over the last one year or so, investors are optimistic that the trend will continue. They further argue that as stocks markets are looking expensive and as there are hope of rate cuts on the anvil, there's even more reason to tilt towards debt.

Well, according to us, it is not the returns of the past but the valuations that count. Stocks have run up alright but they are nowhere close to being very expensive. In fact, at the current valuations, the Sensex is trading at a small premium to its long term average, which in our view cannot be termed as very expensive. Besides, when you consider that corporate profit margins are at multi-year lows and could rebound over the medium term, then the case for equities becomes even stronger. The current markets call for at least a 50%-60% tilt towards equities and the rest towards debt if not more.

Investors in Mutual Funds Moving from Equity to Debt

Now here's a gold story that you may not have heard before. It is reasoned that when giant asteroids crashed into planet earth billions of years ago, one of the elements that emerged out of this collision was the yellow metal gold. And that's it. All the gold that's there above the earth's surface and below it is a result of those collisions that took place billions of years ago. In other words, gold can only be discovered in gold mines and cannot be created from other elements. In fact, even if it can be created, the process is so expensive that one cannot currently make money by selling gold that one creates from other elements.

The point of this short discourse on gold was to highlight the fact that as per a popular website, we might have reached 'Peak Gold'. In other words, all the gold mines that are to be discovered have been discovered and 2015 was the year that could go down as the year gold production maxed. It is argued that all the gold production we have done in the past 20 years has effectively left the cupboards bare. And gold producers are hard at work finding the next big deposit which remains elusive as ever even though exploration budgets increased more than 3 times between 2009 and 2012.

If this is indeed true then aside of the demand, this new supply side scenario could fire up gold prices even more.

Indian stock markets were trading strong today with the Sensex higher by around 100 points at the time of writing. Mid and Small Cap indices were also trading strong, higher by close to 1% each. Amongst sectoral indices, realty and pharma were seen enjoying a good amount of buying interest.

04:56 Investment mantra of the day

"Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid." - Warren Buffett

This edition of The 5 Minute WrapUp is authored by Rahul Shah (Research Analyst).Today's Premium Edition.

Inox Wind: Potential Growth Trap?

What's cooking in the books of Inox Wind? Read more to find...

Read On...

| Get Access

Recent Articles

- All Good Things Come to an End... April 8, 2020

- Why your favourite e-letter won't reach you every week day.

- A Safe Stock to Lockdown Now April 2, 2020

- The market crashc has made strong, established brands attractive. Here's a stock to make the most of this opportunity...

- Sorry Warren Buffett, I'm Following This Man Instead of You in 2020 March 30, 2020

- This man warned of an impending market correction while everyone else was celebrating the renewed optimism in early 2020...

- China Had Its Brawn. It's Time for India's Brain March 23, 2020

- The post coronavirus economic boom won't be led by China.

Equitymaster requests your view! Post a comment on "How Investors Lost Money on the Greatest Event in India's Economic History". Click here!

3 Responses to "How Investors Lost Money on the Greatest Event in India's Economic History"

Mario Braganza

Jul 29, 2016Hi, I need your help.

Inadvertently I deleted y'day's [28 Jul 2016] 5-minute Premium wrap up which I would like you to resend to my email address karlkian@yahoo.co.in

Thanks & Kind regards ... Mario Braganza

89759 52200

Ravi shah

Jul 28, 2016yes Mr RAHUL,If we pay much above the intrinsic value and buy stocks like a perfume and not like groceries then lot of pain may be waiting for us ahead.Your example is quite perfect for overvalued stocks.Thanks

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Narasimmamurthy Radakrishnan

Aug 1, 2016Invaluable information.was never aware that P/E ratios were in excess of 50 in 1992!!THe underlying message is also good.

The adage-"Buy on rumors;sell on news"