MEMBER'S LOGINX

| Invalid Username / Password | ||||||||

| Invalid Captcha | ||||||||

|

||||||||

| Sign Up | Forgot Password? | ||||||||

- Home

- Views On News

- Nov 13, 2023 - Rising Promoter Pledging Trends: Top 5 Stocks to Watch Out

Rising Promoter Pledging Trends: Top 5 Stocks to Watch Out

Promoter pledging is a legal practice where promoters of a company use their shares as collateral for loans.

However, a consistent rise in promoter pledging can be a red flag for investors.

If the company's share price falls, the level of pledging can increase as the lenders demand more collateral. This can happen if margin calls are triggered.

If the company's promoter can't honour these, it may lead to an open market sale of the pledged shares, eroding the value of shares.

While high promoter pledging can be a warning sign, it should not be the sole determinant in investment decisions.

Recent data shows an increasing trend of share pledging among listed companies.

Let's look at the top companies where promoters have pledged their shares recently.

#1 Shilpa Medicare

Shilpa Medicare, a prominent player in the pharma industry, has seen a consistent rise in promoter pledging.

The company, incorporated in 1987, specialises in the production of active pharmaceutical ingredients (APIs) and formulations.

Promoters of Shilpa Medicare have pledged a significant 90.41% of their holdings. This pledge has seen a sharp increase from 12.90% in the previous quarter.

Shilpa Medicare Promoter Pledging

| Quarter Ending | Dec-21 | Mar-22 | Jun-22 | Sep-22 | Dec-22 | Mar-23 | Jun-23 | Sep-23 |

|---|---|---|---|---|---|---|---|---|

| Pledged Promoter Holding (%) | 0.81 | 0.81 | 0.81 | 0.81 | 1.38 | 12.9 | 12.9 | 90.41 |

The company's financial performance has been mixed. In the past five years, the company's revenue has grown from Rs 7 bn to Rs 11 bn while profit has declined.

It even reported a loss in FY23.

Financial Snapshot

| Rs m, consolidated | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| Net Sales | 7,334 | 9,079 | 9,011 | 11,455 | 10,501 |

| Sales growth | -7% | 24% | -1% | 27% | -8% |

| Operating Profit | 1,696 | 2,367 | 2,118 | 2,181 | 1,197 |

| OPM | 23% | 26% | 24% | 19% | 11% |

| Net Profit | 1,123 | 1,562 | 1,478 | 607 | -325 |

| NPM | 15% | 17% | 16% | 5% | -3% |

| Debt to Equity (x) | 0.2 | 0.3 | 0.6 | 0.4 | 0.5 |

| ROE (%) | 9.6 | 12.2 | 10.4 | 3.7 | -1.7 |

| ROCE (%) | 10.5 | 12.4 | 10.7 | 5.9 | 0.8 |

Despite these challenges, Shilpa Medicare holds promise. It has a strong presence in the industry, backed by a robust product portfolio.

In terms of government initiatives, Shilpa Medicare has received approval from the CDSCO (DCGi) for its Tranexamic Acid Spray (Haemostatic Spray).The company has also received a GMP certificate from the UK MHRA.

In its latest concall, the management said that for the next two years, they have a series of complex product launches in addition to the existing products in new countries. This will help improving the company's cash flows.

It also expects two product launches per quarter from the CDMO business.

While Shilpa Medicare presents potential growth opportunities, the consistent rise in promoter pledging and mixed financial performance warrant careful consideration.

Foreign investors (FIIs) also reduced their stake in the most recent quarter to 8.6% from 10.3% earlier.

To know more, check out Shilpa Medicare's latest shareholding pattern.

#2 TTK Prestige

Next on this list we have TTK Prestige, a leading player in the consumer durables industry.

The company, established in 1928, is renowned for its wide range of kitchen appliances.

Promoters of TTK Prestige have pledged 5.95% of their holdings as of September 2023. This is up from 0% in June 2023. The reasons for this increase in promoter pledging are not publicly disclosed, which could be a potential red flag for some investors.

The company's financial performance has been steady.

In recent quarters, the company's kitchen appliances segment has seen a reduced share of wallet and tepid demand due to spending on alternate avenues like automobile, travel, entertainment, and tourism.

The company had also accumulated high-cost inventory in the earlier quarters. This resulted in contraction in gross margins.

Despite all this, TTK has maintained its leadership position in key categories like pressure cookers, cookware, value added gas stoves, induction cook top, kettles, etc and is steadily improving its market share in the mixer grinder segment.

The company has strong growth prospects. As the Indian middle class continues to grow and incomes rise, there is increasing demand for kitchen appliances.

TTK Prestige, the market leader is well-positioned to benefit from this trend, with a diverse product portfolio that includes pressure cookers, cookware, gas stoves, and small kitchen appliances.

Apart from that, the upsurge in real estate development and sales, nuclear family living, changes in consumer behaviour, and acceptance to pay a premium for better products and services, are some more reasons in favour of TTK.

The company's strong market presence and zero debt are positive indicators, but the lower ROE and lack of transparency in promoter pledging could be potential areas of concern.

Financial Snapshot of TTK Prestige

| Rs m, consolidated | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| Net Sales | 21,069 | 20,730 | 21,942 | 27,225 | 27,771 |

| Sales growth | 13% | -2% | 6% | 24% | 2% |

| Operating Profit | 3,213 | 2,908 | 3,568 | 4,616 | 4,063 |

| OPM | 15% | 14% | 16% | 17% | 15% |

| Net Profit | 1,924 | 1,862 | 2,368 | 3,048 | 2,542 |

| NPM | 9% | 9% | 11% | 11% | 9% |

| Debt to Equity (x) | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 |

| ROE (%) | 17.6 | 15.0 | 17.3 | 18.9 | 13.9 |

| ROCE (%) | 24.6 | 18.6 | 22.6 | 25.2 | 18.9 |

#3 Websol Energy System

Websol Energy System, a key player in the solar energy sector, has seen a consistent rise in promoter pledging.

The company was established in 1994 and specialises in the manufacturing of photovoltaic monocrystalline solar cells.

Promoters of Websol Energy have pledged a significant 89.3% of their holdings in the September 2023 quarter. This is a sharp increase from 5.8% in the previous quarter.

The reasons for this increase in promoter pledging are not publicly disclosed, which could be a potential red flag for investors.

On top of this, FIIs have reduced their stake in the company to below 1% from 4% in the June 2023 quarter.

As far as the company's financials go, Websol's balance sheet is still shaky with inconsistent sales and losses reported over the years.

The company posted a loss of Rs 240 million (m) in FY23 as net sales sharply reduced to Rs 170 m from Rs 2.1 billion (bn) in FY22.

Websol has consistently reduced debt and its current debt to equity ratio stands at 0.1x as against 0.6x five years ago.

Financial Snapshot of Websol

| Rs m, consolidated | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| Net Sales | 686 | 1,955 | 1,536 | 2,132 | 172 |

| Sales growth | -63% | 185% | -21% | 39% | -92% |

| Operating Profit | -73 | 137 | 381 | 310 | -98 |

| OPM | -11% | 7% | 25% | 15% | -57% |

| Net Profit | 1 | -194 | 199 | 42 | -79 |

| NPM | 0% | -10% | 13% | 2% | -46% |

| Debt to Equity (x) | 0.6 | 0.6 | 0.2 | 0.2 | 0.1 |

| ROE (%) | -25.8 | 3.3 | 33.1 | 5.3 | -12.4 |

| ROCE (%) | -11.9 | -4.5 | 38.2 | 7.8 | -12.4 |

The company has a strong presence in the solar energy industry and is backed by a robust product portfolio.

Websol has invested in cutting-edge developments to manufacture world-class photovoltaic cells and solar modules at its state-of-the-art facility in Falta, SEZ. The facility comprises a production capacity of 250 MW cells and 250 MW modules.

It has also invested in an R&D (research and development) team focused on maximising equipment utilisation and quality standards with the objective of product customisation.

While Websol Energy presents potential growth opportunities, the consistent rise in promoter pledging and the negative P/E ratio warrant careful consideration.

The company's strong market presence and low debt level are positive indicators, but the lack of transparency in promoter pledging could be a potential area of concern.

#4 Apollo Micro Systems Limited

Apollo Micro Systems specialises in the design, development and manufacturing of electronics and electro-mechanical systems.

Promoters of Apollo Micro Systems have pledged a significant 28.2% of their holdings. This is a sharp increase from 0.9% in the previous quarter.

The reasons for this increase in promoter pledging are not publicly disclosed, which could be a potential red flag for investors.

The company has reported consistent sales and profits for the past couple of years. It also has a lot of tailwinds working in its favour at the moment.

Financial Snapshot of Apollo Micro

| Rs m, consolidated | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| Net Sales | 2,629.75 | 2,459 | 2,031 | 2,432 | 2,975 |

| Sales growth | 19% | -6% | -17% | 20% | 22% |

| Operating Profit | 521 | 503 | 392 | 463 | 649 |

| OPM | 20% | 20% | 19% | 19% | 22% |

| Net Profit | 291 | 140 | 103 | 146 | 188 |

| NPM | 11% | 6% | 5% | 6% | 6% |

| Debt to Equity (x) | 0.4 | 0.3 | 0.4 | 0.4 | 0.4 |

| ROE (%) | 10.8 | 4.7 | 3.4 | 4.7 | 5.7 |

| ROCE (%) | 12.5 | 10.6 | 7.6 | 8.7 | 10.7 |

Last month, the company announced an ambitious capital expenditure plan of Rs 1.5 bn to establish a defence equipment manufacturing facility at Hardware Park in Hyderabad.

The proposed new units will expand the existing infrastructure by an impressive 300,000 square feet and will serve as a home for a defence electronics and electro-mechanical manufacturing facility, capable of handling bulk production.

Apollo Micro Systems also announced significant agreements with the Defense Research and Development Organisation (DRDO), marking a significant milestone in their ongoing partnership.

The company is actively engaged in discussions with various international companies interested in producing their goods under the 'Make in India' initiative, and this state-of-the-art facility will be utilized to fulfil their manufacturing needs.

While Apollo Micro Systems presents potential growth opportunities, the consistent rise in promoter pledging and the high P/E ratio warrant careful consideration.

The company's strong market presence and low debt level are positive indicators, but the lower ROE and lack of transparency in promoter pledging could be potential areas of concern.

#5 Polyplex Corporation

Last on the list is Polyplex Corporation, a leading player in the plastic products industry. The company specialises in the manufacturing of PET films.

Promoters of Polyplex Corporation have pledged all their shares in the most recent September 2023 quarter. This pledge is a sharp increase from 0% in the previous quarter.

This pledging out of the blue has raised some concerns among investors.

Earlier this year, the promoters of Polyplex Corporation agreed to sell a 24.2% stake in the firm to Dubai-based AGP Holdco.

The deal was valued at Rs 13.8 bn at that time and includes a binding term sheet as well as provisions for put and call options. This would allow AGP Holdco to increase its stake in the future.

However, it was announced last month that the deal value will be revised downward to Rs 11.9 bn. All this has created a degree of uncertainty in the market about the company's future.

The company's EPS is also declining consistently. If you were to look at the company's performance over last eight quarters, EPS has been falling since September 2022.

However, Polyplex does have a strong presence in the plastic products industry and is backed by a robust product portfolio.

The company has consistently generated strong operating cash flow over the past decade, thanks to its high-capacity utilisation and its presence in the less volatile BOPET segment.

Financial Snapshot of Polyplex

| Rs m, consolidated | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| Net Sales | 45,699 | 44,871 | 49,183 | 66,244 | 76,523 |

| Sales growth | 28% | -2% | 10% | 35% | 16% |

| Operating Profit | 8,949 | 8,421 | 12,759 | 14,359 | 10,424 |

| OPM | 20% | 19% | 26% | 22% | 14% |

| Net Profit | 3,300 | 2,820 | 5,118 | 5,688 | 3,484 |

| NPM | 7% | 6% | 10% | 9% | 5% |

| Debt to Equity (x) | 0.3 | 0.3 | 0.2 | 0.3 | 0.2 |

| ROE (%) | 22.0 | 17.0 | 28.4 | 30.3 | 18.1 |

| ROCE (%) | 19.7 | 17.9 | 26.5 | 29.1 | 17.5 |

While Polyplex Corporation presents potential growth opportunities, the recent rise in promoter pledging warrants careful consideration by investors.

The company is expected to showcase improved financial performance due to stabilising input costs and the re-negotiation of old contracts. The company is also benefiting from a rise in demand, which is creating favorable market conditions.

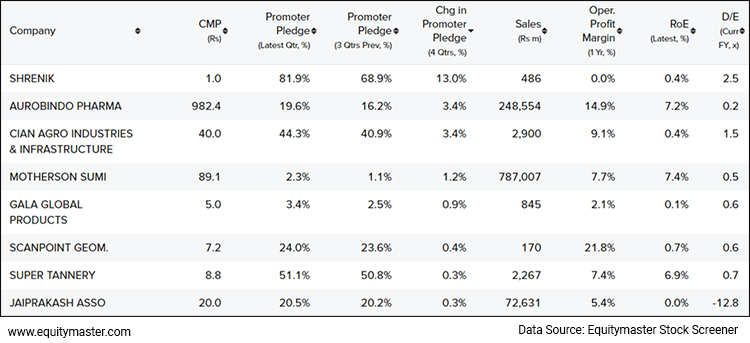

Snapshot of Companies with High Promoter Pledging

Here's a snapshot of companies that have seen promoter pledging for the past four quarters.

Since promoter activity interests you, check out other screens on Equitymaster's powerful stock screener.

- Stocks with High Promoter Pledge in India

- Promoters Decreasing Stake for 4 Consecutive Quarters

- Promoters Increasing Stake for 4 Consecutive Quarters

Investment Takeaway

In conclusion, tracking promoter activities, particularly share pledging, is crucial in stock analysis.

While share pledging is a legal and common practice for securing funds, a consistent rise can signal potential financial distress.

It's important to understand the context. If funds raised through pledging are used for income generation, it's less concerning than if used for personal purposes.

A significant drop in share price can trigger margin calls, potentially leading to an open market sale of pledged shares, further eroding share value.

Therefore, alongside financial health, tracking promoter activities is vital when shortlisting stocks for your portfolio.

Stay informed, stay cautious, and happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here...

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "Rising Promoter Pledging Trends: Top 5 Stocks to Watch Out". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!