MEMBER'S LOGINX

| Invalid Username / Password | ||||||||

| Invalid Captcha | ||||||||

|

||||||||

| Sign Up | Forgot Password? | ||||||||

- Home

- Todays Market

- Indian Stock Market News August 20, 2016

Global Markets End on a Mixed Note Sat, 20 Aug RoundUp

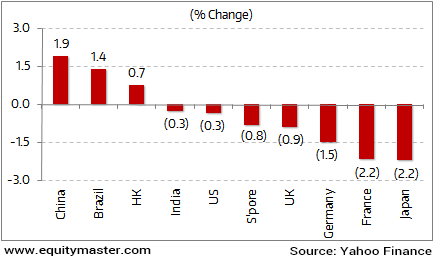

Global indices closed on a mixed note for the week. China (up 1.9%) and Brazil (up 1.4%) were among the biggest gainers. Japan (down 2.2%) and France (down 2.2%) were the top losers in the pack.

European share markets posted their biggest weekly loss in two months, while the US market edged lower, led by declines in utility shares as investors weighed prospects for an interest rate increase in the coming months.

The minutes of Federal Open Market Committee (FOMC) meeting held last month released this week signaled that doors are still open for 2016 interest rate hike. This comes as The US central bank's policymakers expect that an interest rate increase will be needed soon. However, the general agreement is that more data will be looked upon before such a move becomes reality.

The minutes showed that members of the US central bank's rate-setting FOMC were generally upbeat about the economic outlook and labour market. However, on the other hand, several said a slowdown in the future pace of hiring in the US would act as a hindrance for a near-term hike. Notably, several policymakers expressed concern that low-interest rates could hurt financial stability. The next big chance to glean insight from US central bank officials comes in a week's time, with Fed chief Janet Yellen due to speak at an annual gathering of central bankers in Jackson Hole, Wyoming on 26 August.

Coming to Europe, The UK budget surplus decreased in July despite higher corporate tax receipts, suggesting that the Brexit vote is likely to reduce the pace of improvement in public finances going forward. The public sector net borrowing, excluding public sector banks, was a surplus GBP 1 billion in July 2016. The surplus decreased by GBP 0.2 billion from July 2015. Economists had forecast a bigger surplus of GBP 1.9 billion. The budget usually registers surplus in July, as it is a key month for tax receipts.

Back in Asia, China's industrial output for July grew 6% YoY July retail sales grew a respectable 10.2% on year. Similarly, fixed asset investment (FAI) for the January-to-July period rose 8.1%. China's statistics bureau mentioned that the economy remained under downward pressure amid a period of adjustment. The mainland has been working to transition its economy toward domestic consumption and away from reliance on investment- and manufacturing-led growth.

In Hong Kong, the share market had a belatedly positive reaction to China's confirmation that the Shenzhen-Hong Kong Stock Connect program will proceed later this year. China on Tuesday gave the green light to a stock-trading link between Hong Kong and Shenzhen, which is expected to boost trading flows into both markets. Under the program, global investors would be able to buy Shenzhen stocks and Shenzhen investors would be allowed to buy Hong Kong stocks.

Japan's Nikkei remained choppy and was down by 2.2% this week as investors remained wary over the strength of the yen, which has taken a heavy toll on exporters.

Oil prices surged this week on expectations of revived talks to freeze output levels. Global benchmark Brent crude touched an eight-week high of US$51.1 on Friday and was last trading at US$48.5.

In currency markets, The U.S. dollar was near an eight-week low against major currencies in the wake of minutes from the Federal Reserve's July meeting published on Wednesday showing policymakers were unlikely to raise interest rates soon.

Back home, the Indian indices ended with a negative zone. Weak global cues, profit booking and a weak rupee subdued the Indian equity markets. Investors also turned cautious ahead of the announcement of the next RBI governor. The BSE Sensex was down by 0.3% for the week.

Key World Markets During the Week

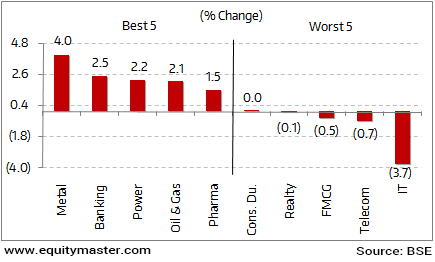

On the sectoral indices front, Metal and Banking stocks led the gainers this week. On the other hand, stocks from IT and Telecom witnessed selling pressures.

BSE Indices During the Week

Now let us discuss some key economic and industry developments during the week gone by.

Wholesale price inflation accelerated more than expected in July and hovered near a two-year high. This was seen mainly on the back of rising food prices, which rose to double digits for the first time since December 2013. Notably, the wholesale price index (WPI) nearly doubled and rose 3.55% from a year ago. This rise was as against a 1.62% rise witnessed in June. It was also higher than the expected 2.5% wholesale inflation. Primary articles inflation rose 9.3% and manufactured product index grew 1.8%. On the other hand, fuels inflation fell 1%. Core inflation stood at 0.1% after 16 months of disinflation. Most of the increase was attributed to food inflation. Food inflation spiked to a 30-month high of 11.8%.

Talking about inflation, the standard GST rate could be closer to 22% when the tax is rolled out. This is as against the widely touted figure of 18%. The GST's rollout could have a temporary inflationary impact on the economy. One must note that while the GST act has been approved by most of the leading parties, the tax is far from a done deal yet. Half the states still need to approve the legislation. Along with this, the GST council, a very important part of the process, will also need to be set up. It will be the job of the Council, which will be two-thirds represented by the states, to decide on the GST rate after which three GST Bills (Central GST, Integrated GST and State GST) mentioning the actual rates will be sent to Parliament and state assemblies for approval. Vivek Kaul, editor of Vivek Kaul's Diary, has brilliantly explained what you probably did not hear about GST from the mainstream media. He's stated all of it in a special report titled 'GST & You: What the Media DID NOT TELL YOU About the GST'.

Moving to banking space, Foreign and public sector banks (PSBs) have lost share of primary banking relationships to new private banks. As per the reports by industry body Federation of Indian Chambers of Commerce and Industry), IBA (Indian Banks' Association) and BCG (Boston Consulting Group) the share of primary banking relationships for PSBs, excluding SBI and its associates, fell from 35% in 2013 to 30% in 2016 while that of foreign banks fell from 13% to 6%. At the same time, the share of private banks during the period has risen from 29% to 36%. This comes amid the fact that corporates are increasingly consolidating towards two bank accounts. The reason for an increase in the share of private banks is that they have better transaction banking propositions, which determine primary banking relationships. They are more aggressive in marketing current accounts, payments and collection solutions than PSU banks. The report also reveals that digital transactions have increased by 70% over the last year while bank branches have decreased.

Crude oil witnessed buying interest this week. The uptrend was seen on the back of higher demand in the US and possibility of an accord by the OPEC on output freeze. The commodity surged on comments from the Saudi oil minister about potential action to stabilize prices. Further, the forecasts by International Energy Agency (IEA) that crude oil markets would rebalance in the next few months aided the rally in crude oil. Recently Saudi energy minister Khalid al-Falih lent more credibility to the idea of controlling the downtrend on oil prices. He stated that the OPEC might consider taking action if oil prices remained low. Along with the above announcement, the IEA stated that the world will consume less oil next year than previously thought. It estimated global oil demand growth to slow from 1.4 millions of barrels a day in 2016 to 1.2 million barrels a day in 2017. This was noted 100,000 barrels below its previous forecast. Do read what Richa Agarwal, research analyst at Equitymaster, has to say on the future prospects of crude oil prices.

Movers and Shakers During the Week

| Company | 10-Aug-16 | 19-Aug-16 | Change | 52-wk High/Low |

|---|---|---|---|---|

| Top Gainers During the Week (BSE Group A) | ||||

| Piramal Enterprises | 1,604 | 2,037 | 27.0% | 1,960/805 |

| Indian Bank | 192 | 229 | 19.3% | 237/76 |

| Hindustan Copper | 59 | 70 | 18.0% | 69/42 |

| SBI | 228 | 256 | 12.4% | 286/148 |

| Jain Irrigation | 73 | 81 | 11.7% | 83/47 |

| Top Losers During the Week (BSE A Group) | ||||

| Unitech | 6 | 5 | -17.4% | 9/3 |

| Aditya Birla Nuvo | 1,566 | 1,298 | -17.1% | 2,364/685 |

| Strides Shasun Ltd | 1,159 | 984 | -15.1% | 1,412 / 848 |

| Jaiprakash Power | 5 | 5 | -10.2% | 8/4 |

| Thermax Ltd | 904 | 837 | -7.4% | 1,061 / 691 |

Now let us move on to some of the key result announcements during the week.

Power Grid Corporation of India (PGCIL) reported its results for the quarter ended June 2016. The company's net profit grew by 32% YoY to Rs 18 billion during the quarter. The profits grew on the back of robust project capitalization of Rs 297 billion in the trailing four quarters. However, the company could only capitalize Rs 25 billion in the quarter ended June. There were minor delays in the completion of Champa-Krukshetra and second pole of Agra-NE line. Both the lines are now expected to be completed in the second quarter of FY17. Further, the revenues from telecom and consultancy business grew by 25% YoY and 35% YoY during the quarter. Increasing competitive scenario and success in Tariff Based Competitive Bidding Projects (TBCB) will be the key things to watch out for going forward.

Hindalco Industries reported its results for the quarter ended June 2016. The topline declined by 11.4% YoY, the bottomline increased by 379% YoY during the quarter. Aluminium EBITDA is up by 64% YoY on strong volumes and robust operating performance. However, Cathode production declined during the quarter on the back of planned maintenance shutdown. Novelis, Hindalco's subsidiary also posted a good performance with adjusted EBITDA growing by 26% YoY. The subsidiary registered a 15% YoY increase in automobile sheet shipment volumes. However, it is important to note that aluminium companies have started feeling the pressure of cheap imports. Unlike the steel industry, which has managed to get strong support from the government recently, the domestic aluminium industry has not been able to make itself heard. Similarly, with the rising aluminium prices, we can expect the growing supply in the coming months with the restarting of idle Chinese smelters and addition of new capacities. Therefore going forward, aluminium prices could come under pressure.

And here are some of the key corporate developments in the week gone by.

Tata Power's subsidiary of Tata Power Solar has commissioned a 100 MW solar project under local content requirements in Anantapur, Andhra Pradesh. This 100 MW plant is the largest to date in India built using domestically manufactured solar cells and modules. Reportedly, the project has been developed for India's largest utility NTPC. Tata delivered the project three months ahead of schedule according to a company statement. Notably, the plant is expected to generate nearly 160 million units of energy per year. Considering power sector's several headwinds, we have discussed the challenges faced by Tata Power (Subscription Required) in one of our premium editions of The 5 Minute Wrap Up. Further, the key highlights of the project included the innovative design of Balance-of-System (BoS) and cabling, along with optimized selection of evacuation systems.

Bharat Heavy Electricals Ltd (BHEL) has secured an order for setting up of Solar Photovoltaic (SPV) Power Plants on engineering, procurement and construction basis from West Bengal State Electricity Distribution Corporation (WBSEDC). Reportedly, the order at Rs 1.7 billion for installation of 30 MW (3x10 MW) SPV was placed in a letter of intent by WBSEDC. Notably, BHEL also bagged EPC orders from Neyveli Lignite Corporation and Bharat Electronics for setting up of a 65 MW SPV Power plant in Tamil Nadu this year. Moreover, a 15 MW SPV Power plant in Telengana is currently under execution. BHEL had earlier bagged EPC orders from NTPC for a 50 MW SPV plant in Andhra Pradesh and Madhya Pradesh each. This also takes the company further into the domain of SPVs power plants, a direction that the BHEL intends to increasingly foray into over the long term.

L&T has been identified as Implementation Partner to convert Nagpur into the country's first large-scale integrated Smart City as per a Letter of Intent from Maharashtra government. This is in line with the government's vision to use vanguard technology for creating smart solutions to improve quality of life of citizens. The scope of work in Phase 1 for L&T's Smart World Communications business vertical, which is a part of L&T Construction, will cover laying of 1,200 km of optical fiber network backbone, creating 136 City Wi-Fi hotspots at key locations, establishing 100 digital interactive kiosks and developing city surveillance systems with 3800 IP based cameras.

Hindalco's Novelis unit will launch a bond sale in the US to raise as much as US$1.1 billion to refinance debt. The money will go toward refinancing bonds that mature in December 2017. The base size of the issue is $550 million with an option to retain oversubscriptions. The company plans to take advantage of demand for Indian bond in global market. Demand for debt instruments of Indian companies has gone up after the global bond market was roiled by Brexit and amid a climate of zero interest rates as central banks looks to bolster faltering economies.

And here's an update from our friends at Daily Profit Hunter...

Indian Indices Skid Downward

For information on how to pick stocks that have the potential to deliver big returns, download our special report now!

Read the latest Market Commentary

Indian Share Market Update: Top Gainers and Losers

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "Global Markets End on a Mixed Note". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!