MEMBER'S LOGINX

| Invalid Username / Password | ||||||||

| Invalid Captcha | ||||||||

|

||||||||

| Sign Up | Forgot Password? | ||||||||

- Home

- Views On News

- Dec 5, 2023 - 5 Most Undervalued Smallcap Stocks to Watch Out as 2024 Begins

5 Most Undervalued Smallcap Stocks to Watch Out as 2024 Begins

Over the past few days, stocks have been very good to investors. They've been scaling new heights, capitalising on the bullish market sentiment.

Smallcaps in particular, have shot up.

There's been no shortage of dinner table stories. Stocks rising by 20%, 30% or even 50% in a matter of days has become the common norm.

Amid the bullishness in the market, there are some decent quality stocks that look undervalued by their valuation ratios.

Let's take a look at five such smallcap stocks.

#1 Chennai Petroleum Corporation (CPCL)

First on the list is Chennai Petroleum Corporation.

The company is engaged in the business of refining crude oil and manufacturing lubricating oil additives.

Being a part of the Indian Oil Corporation (IOC) group and the only south Indian refining company of IOC, it has operational benefits with respect to crude oil import.

The company's shares are currently trading at single-digit price-to-earnings (P/E) ratio of 3.5x and price-to-book value (P/BV) of 1.3x.

Being a 'refining-only' company, it has limited pricing flexibility and volatile profit margins. This could justify the low valuations.

However, Chennai Petroleum Corporation is a hidden treasure that is yet to be explored by investors.

Its locational advantage ensures there is low demand risk, which helps the company strengthen its presence in the southern market.

It has also demonstrated consistent improvement in financial performance in the last five years. The revenue has grown at a CAGR of 15.4%, driven by healthy growth in demand and volumes.

It also became profitable and reported its highest-ever net profit of Rs 35 billion (bn) in the financial year 2023.

The company reduced its debt-to-equity ratio from 2.2x in the financial year 2020 to 0.3x in the financial year 2023.

Its return on equity (RoE) and return on capital employed (RoCE) stand high at 54.5% and 59.5%, respectively.

Foreign institutional investors (FII) have also been increasing their stake in the company, taking their stake up from 2% to 11% in the last three years.

Chennai Petroleum Corporation currently has a refining capacity of 10.5 metric tonnes per annum (MTPA). It is adding another 9 MTPA along with IOC. The company's investment will be around Rs 25 bn, which it plans to fund through equity and debt.

It also started paying dividends to its shareholders from the last two years with an average dividend payout and dividend yield of 6.8% and 5.7%, respectively.

Given its improving financial performance and growing demand for petroleum products, the company's share price could catch up to its valuations soon.

To know more, check out Chennai Petroleum Corporation's financial factsheet and latest quarterly results.

#2 Bodal Chemicals

Second on the list is Bodal Chemicals.

The company is India's leading integrated dyestuff company and the largest domestic manufacturer of dye intermediaries.

It has a market share of 20% in the domestic dye intermediaries market and 13% in the dyestuffs market. The global market share is 6% and 3%, respectively, in the dye intermediaries and dyestuffs market.

The company has state-of-the-art research and development (R&D) laboratories that it uses to develop new products and processes. Recently, it also added benzene derivatives to its product portfolio.

Bodal Chemicals has also invested Rs 4 bn in a greenfield project to increase the capacity of speciality benzene downstream products. This is expected to be operational by December 2023.

Coming to its financial performance, the company's revenue has grown at a CAGR of 8.5% in the last three years, driven by capacity expansions. The net profit fell slightly due to high input costs.

The company also pays consistent dividends to its shareholders, and its P/BV ratio stands at 0.9x, much lower than the industry average and its peers.

With the new greenfield project expected to commence production, the company will benefit from higher production, which could improve sales and profit growth.

To know more, check out Bodal Chemicals' financial factsheet and latest quarterly results.

#3 International Conveyors

Next on the list is International Conveyors.

The company is engaged in the manufacturing and marketing of solid woven PVC-covered conveyor belts. These belts are mainly used in underground mines for the transportation of minerals.

It produces electricity through wind energy through five windmills installed in five different states.

The shares of the company are currently trading at a P/E of 12.1x and a P/BV of 2.4x, which is lower than the industry average P/E of 38.6x and 4.5x, respectively.

The current valuations are also lower than its 5-year average PE of 24.9x and 3-year average PE of 23.8x.

In the last five years, the company's revenue has grown at a CAGR of 19.6%, driven by higher export orders. The company has also turned profitable and reported a net profit of Rs 287 million (m) as against a loss of Rs 57 m in 2019.

The net margin expanded from 6.5% to 13.4% in the last five years. As a result, the RoE and RoCE have improved to 13.4% and 19.2% respectively.

The company operates in a niche segment. This means it has less competition, which helps take advantage of the growth in underground mining operations and commands premium pricing.

Another key factor is that the company has zero debt, which means low fixed financial obligations, which leaves more money to invest in capex and distribute dividends. With no major capex planned in the medium term, the company has paid higher dividends to its shareholders in the past and the trend could continue.

Promoter buying is also on the rise. Since December 2020, the company's promoters have increased their stake from 61.7% to 71%.

To know more, check out International Conveyor's financial factsheet and latest quarterly results.

#4 Tinna Rubber & Infrastructure

Fourth on the list is Tinna Rubber & Infrastructure.

The company is engaged in the conversion of end-of-life tyres into crumb rubber and steel wires. Its products include crumb rubber modifier, crumb rubber modified bitumen, polymer modified bitumen, bitumen emulsion, and cut wire shots.

Being the largest manufacturer of crumb rubber, it has several reputed companies as its clients, including MRP, Apollo, Ceat, JK Tyres, and Mangalore Refinery.

The company's current P/E ratio stands at 41.8x, which is lower than the industry average but way higher than its historical average.

In the last five years, the company's revenue has grown at a CAGR of 17.9%, owning to healthy demand from its existing and new customers. It reported a net profit of Rs 218 m as against a net loss of Rs 39 m in 2020.

The net profit margin has also improved consistently, along with return ratios. The RoE and RoCE currently stand at 22.7% and 30.6% respectively.

At present, the company has 80 thousand metric tonnes (MT) of tyre crushing capacity. It plans to increase it to 2.5 million MT by the end of the financial year 2027.

With growing demand for crumb rubber, the capacity expansion couldn't have come at a better time.

All these factors indicate that the smallcap stock has a lot of potential for growth.

To know more, check out Tinna Rubber and Infrastructure's financial factsheet and latest quarterly results.

#5 Tamil Nadu Newsprint

Last on the list is Tamil Nadu Newsprint and Papers.

The company is engaged in manufacturing paper and paper boards best suited for the printing, writing, and packaging industry.

It also produces cement and generates power through wind energy for captive use.

Despite being the third largest player in the paper industry in India, the company's valuations are low when compared to its peers.

The current P/E and P/BV ratios stand at 5x and 0.9x, respectively, whereas the industry average P/E and P/BV are 11.7x and 1x, respectively. Its 3-year and 5-year average PE also stands at 8.5x.

In the last three years, the company has reported a sales growth (CAGR) of 23.2%, driven by high demand and growth in sales realisations. Its net profit has also improved to Rs 3.8 bn as against a loss of Rs 651 m three years ago.

Due to improvement in net margins, the return ratios have improved as well with ROE coming in at 20% and ROCE at 26.1%.

Repayment of debt has led to a fall in the debt-to-equity ratio to 0.5x from 1x.

Apart from a strong financial performance, the company has a strong distribution network and access to diversified raw material sources which reduces the raw material availability risks.

Given the company's major contribution from paper products, it stands to benefit from the growing demand for paper.

To know more, check out Tamil Nadu Newsprint and Papers' financial factsheet and latest quarterly results.

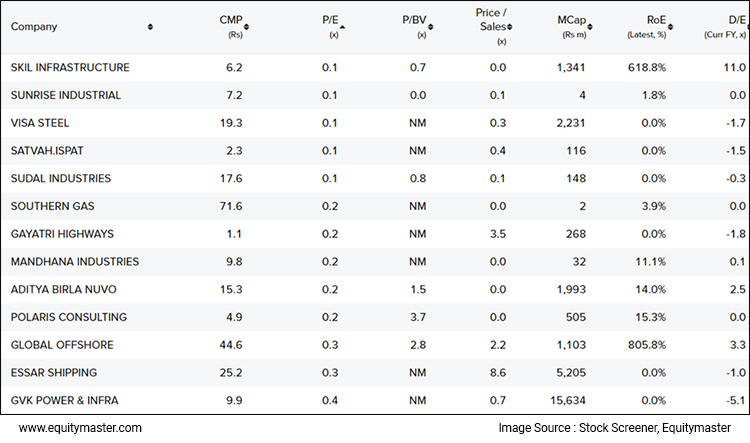

Snapshot of Undervalued Smallcap Stocks

Here's a table showing some other smallcaps that look undervalued right now

Since you're interested in undervalued stocks, check out Equitymaster's stock screener which has a separate section for valuations.

Here are some popular screens

Happy Investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here...

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "5 Most Undervalued Smallcap Stocks to Watch Out as 2024 Begins". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!